What does lower oil mean for infrastructure?

Supply glut: a driving force for plunging oil prices

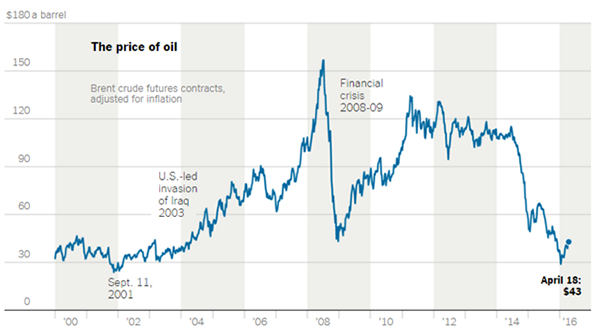

Brent crude oil prices are down more than 53% from their levels two years ago (figure 1), falling to about US$49 a barrel as of 7 July 2016. Our analysts agree that it has been supply, not demand, that has been driving energy prices down. The shale boom in the US saw a surge in production in recent years, while major producers like Saudi Arabia have also dramatically increased their oil supply. We expect that it will take a while to work through the excess supply.

Figure 1: Oversupply has seen the price of oil plunge

Source: Bloomberg, AMP Capital. Data as at 22 June 2016.

On the demand side, there are so many new technologies, especially when it comes to automobiles (such as fuel-cell motor technology or electric cars) which have reduced oil consumption and had a dramatic impact on the oil market. As such, the regular demand response hasn’t played out in the market. Typically, when oil prices decline over 50%, there is an implied demand response for price elasticity. In other words, when the price drops, demand shoots higher. However, this time, demand hasn’t increased as much as expected in response to the sharp price drop.

What does this mean for the midstream infrastructure sector?

The midstream supply chain of the energy sector involves gathering systems, transportation systems (by pipeline, rail, barge, oil tanker or truck), terminals and storage of crude or refined petroleum products. Midstream assets are typically underpinned by fixed-fee or minimum volume commitment contracts which avoid commodity exposure as oil/gas prices are typically ‘passed through’ in the contract to the end-users (such as a refinery). Given the stable and transparent nature of cash flows, midstream assets are highly sought-after infrastructure investments.

Shorter return horizon

We expect that environmental policy responses over the next decade such as the Paris Climate Change Agreement will curb – and ultimately lead to a significant decrease in – demand for fossil fuel, most notably coal (the most intensive).

The degree of structural change means that investment in energy, transport and associated infrastructure long-life assets will be challenged as asset life will be shortened (requiring higher returns) or potentially lead to assets being ‘stranded’ in the future. This is likely to favour fossil fuel companies that can respond quickly to incremental changes in demand, such as US oil and gas shale companies.

Ultimately, there is a greater risk to growth options in energy and infrastructure sectors which rely on long-life assets. The energy industry is used to having investments over a longer period of 20 to 25 years. But when there’s a risk that what’s built now may not be around in 20 years’ time, investors may want to see a return on capital within a shorter 10-15 year timeframe.

Outlook

The decline in oil prices has significantly dampened investor sentiment about oil-exporting emerging market economies, and could lead to substantial volatility in financial markets, as was observed in a number of countries in the last quarter of 2014. However, declining oil prices also present a significant window of opportunity to reinvigorate reforms and diversify oil-reliant economies. Over the longer term, adjustment will take place from both conventional and unconventional sources through cancellation of projects. While supply is likely to be truncated, ongoing demand will be underpinned by recovering global activity in line with broader demographic trends.

The oil price shocks of the 1970s serve to remind us of the potential impact that energy prices can have on economies and markets. While the global economy is no longer as sensitive to oil prices, investors designing portfolios to fund consumption goals in the future do still need to pay close attention to the energy price sensitivities of their strategies.

Source: AMP Capital

Important note: While every care has been taken in the preparation of this article, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) makes no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This article has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this article, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided.